What Credit Score Do You Need to Finance a Car

What credit score do you need to finance a car? The most honest answer is that there is no single number that guarantees approval.

If you want the wider context first, our used car financing guide for Vancouver explains how approval, affordability, and planning fit together.

In Canada, your credit score matters, but it is only one part of the picture. In many cases, buyers with stronger credit have an easier time qualifying and may receive better financing terms. At the same time, many people with fair credit, limited credit history, or past financial problems still manage to finance a vehicle. The final decision often depends on a mix of factors, including your income, job stability, debt level, down payment, and the vehicle you want to buy.

Many buyers search for one “minimum score” and assume the answer is simple. In practice, it usually is not. A person with a lower score but stable income and a reasonable budget may be in a better position than someone with a higher score who is already stretched too thin.

For used-car buyers, it helps to think beyond the number itself. Approval matters, but so do the rate, the monthly payment, the total cost over time, and whether the vehicle actually fits your budget. A financing offer only makes sense if it supports reliable transportation without creating more financial pressure.

This guide explains how credit scores affect car financing, what score ranges usually mean, what lenders look at besides your score, and what you can do if your credit is fair, poor, or still being built. For a broader step-by-step overview, you can also read Everything You Need to Know About Financing Used Vehicles.

The Short Answer: There Is No One Magic Credit Score

If you want the short answer first, here it is: there is no universal credit score that every lender uses for car financing.

Some buyers are approved with strong credit and receive better terms. Others are approved with average or weaker credit because the rest of their application is solid. That is why it is more useful to think in score ranges than to look for one exact cutoff point.

A simple credit score range guide for car financing

| Credit Score Range | What It Often Means for Car Financing |

|---|---|

| 760+ | Very strong credit profile. Buyers in this range are often in the best position for more competitive rates and easier approval. |

| 660–759 | Generally a solid range for mainstream financing. Approval is often more straightforward when the rest of the file is stable. |

| 600–659 | Still possible in many cases, but terms may be less favourable and lenders may review the file more carefully. |

| 550–599 | Approval may still be possible, but buyers in this range often face stricter conditions, higher rates, or requests for more supporting information. |

| Below 550 | Financing can be more difficult, but not always impossible. Approval often depends heavily on income, down payment, overall debt load, and lender type. |

These ranges are general guidance, not promises. Different lenders use different standards, and one may view the same application differently from another.

Your score also does not tell the full story. A buyer with a lower score but steady income and low debt may be in a better position than someone with a higher score who is already financially stretched.

What most buyers should take away from these ranges

A practical way to read the chart is this:

- A score in the mid-600s or above usually puts you in a stronger position.

- A score in the low-600s may still be workable, but the financing terms may become more expensive.

- A score below that does not automatically end your options, but other parts of your application start to matter much more.

In other words, the score helps shape the conversation, but it does not decide the entire outcome by itself.

How Credit Scores Affect Car Financing in Canada

A credit score matters because it helps a lender estimate risk. It is not a full picture of your finances, but it does give signals based on your borrowing history.

That is why buyers with stronger scores often have an easier time getting approved and may receive better terms. At the same time, the score is only one part of the decision. A lender also looks at whether the payment fits your income, current debts, and the vehicle itself.

What a credit score tells a lender

A credit score is built from information in your credit history. In simple terms, lenders may see a stronger score as a sign of more consistent credit management, while a weaker score may point to missed payments, heavy credit use, or past financial strain.

Some of the common signals behind a credit score include:

- your payment history

- how much of your available credit you are using

- how long you have had credit accounts open

- the mix of credit products you use

- recent applications for new credit

- serious negative events such as collections or bankruptcies

Why a higher score usually helps

A higher score can improve both approval chances and the quality of the financing offer.

Buyers with stronger credit may have:

- access to more lender options

- a better chance of approval on standard terms

- more competitive interest rates

- more flexibility on loan structure

- less need for extra conditions or explanations

Even when approval is possible with weaker credit, a higher rate can raise the total amount paid over the life of the loan.

Why a lower score does not always mean no

A lower score can make financing more difficult, but it does not always mean a hard stop. Some lenders still consider these files, especially when the rest of the application is strong.

That can include:

- stable full-time employment

- income that supports the payment

- a reasonable down payment

- limited existing debt

- a realistic vehicle choice

- recent signs of financial recovery or consistency

Why used-car buyers should think beyond approval

For used-car buyers, the goal should not be approval at any cost. The better goal is approval on terms that fit your real budget.

A vehicle should not just be financeable. It should also be affordable to keep once insurance, fuel, maintenance, and repair risk are considered.

What Credit Score Is Considered Good for a Car Loan?

Many buyers ask this because they want to know whether their score is good enough before they apply. In practical terms, a good credit score for a car loan is one that puts you in a stronger position for mainstream financing, more lender options, and more competitive rates.

That does not mean anything below that is automatically bad, and it does not mean anything above that guarantees an ideal offer. It simply means the application is often easier to place when the score shows a more stable borrowing history.

Good, fair, and poor credit in practical terms

A simple way to think about it is this:

- Good credit usually means you are more likely to qualify through standard lending channels on more reasonable terms.

- Fair credit often means approval is still possible, but the lender may be more cautious and the rate may be higher.

- Poor credit usually means the file needs more support from other factors such as income, down payment, or job stability.

These categories are useful because they reflect what buyers often experience in real financing situations.

What many buyers should realistically expect by score band

Around 660 and above

This range often gives buyers a stronger starting point. It usually means a smoother approval process, more lender choices, and a better chance of competitive terms.

Around 600 to 659

This range is often workable, but it can be more sensitive. A buyer here may still qualify, especially with steady income and manageable debt, but the lender may review the file more closely.

Below 600

This range can be more difficult, but it is still not the same as impossible. At this point, lenders often become more focused on the full risk picture, including:

- stable employment

- enough income for the proposed payment

- a modest or meaningful down payment

- lower overall debt pressure

- a more realistic vehicle choice

Why buyers should focus on financing strength, not just score labels

A more useful question is whether your overall financing profile is strong enough for the kind of vehicle and monthly payment you want. It also helps to compare your budget against real options in the current used car inventory.

That is why score labels should be used as planning tools, not as final judgments.

What Lenders Look At Besides Your Credit Score

A credit score matters, but it is not enough on its own to explain whether a financing application is strong or weak.

Lenders are not only asking whether you have used credit well in the past. They are also asking whether the proposed loan makes sense today. That is why two buyers with similar scores can still end up with different results.

Income

Income is one of the first things a lender will look at because it helps show whether the proposed payment is realistic.

Lenders may look at:

- gross monthly income

- whether the income is stable and ongoing

- how much room is left after housing, debt, and living costs

- whether the requested payment fits the overall budget

Employment stability

Employment history often matters almost as much as income itself.

Lenders may pay attention to:

- how long you have been at your current job

- whether you are full-time, part-time, contract, or self-employed

- whether you are still in a probation period

- whether your work history shows stability or frequent disruption

Debt load

Your current debt matters because it affects how much financial room you actually have for another payment.

Common debt considerations include:

- credit-card balances

- lines of credit

- personal loans

- student loans

- other auto loans

- monthly housing obligations

A buyer with moderate credit but manageable debt may be in a better position than a buyer with a better score but very little room left in the budget.

Down payment

A down payment can strengthen an application because it lowers the amount being financed and reduces the lender’s risk.

A down payment may help by:

- lowering the amount borrowed

- reducing the monthly payment

- making approval easier in some cases

- offsetting part of the lender’s risk

- improving the overall affordability of the vehicle

Vehicle type, age, and price point

Lenders also look at the vehicle. Older vehicles, high-mileage vehicles, or vehicles priced outside what the lender sees as practical may create more caution.

This is one reason a realistic vehicle target matters so much. A modest, reasonably priced vehicle may be easier to finance than a more expensive one, even for the same buyer.

Past credit problems

Past financial events can still matter even if your score has started to recover.

Lenders may look beyond the score itself and review whether your report shows:

- missed payments

- accounts in collections

- past repossessions

- consumer proposals

- bankruptcy history

- recent patterns of late payment

Why the full file matters more than many buyers realize

A stronger application usually comes from a combination of factors working together. Credit score is part of that, but income, debt, employment, down payment, and vehicle choice also matter.

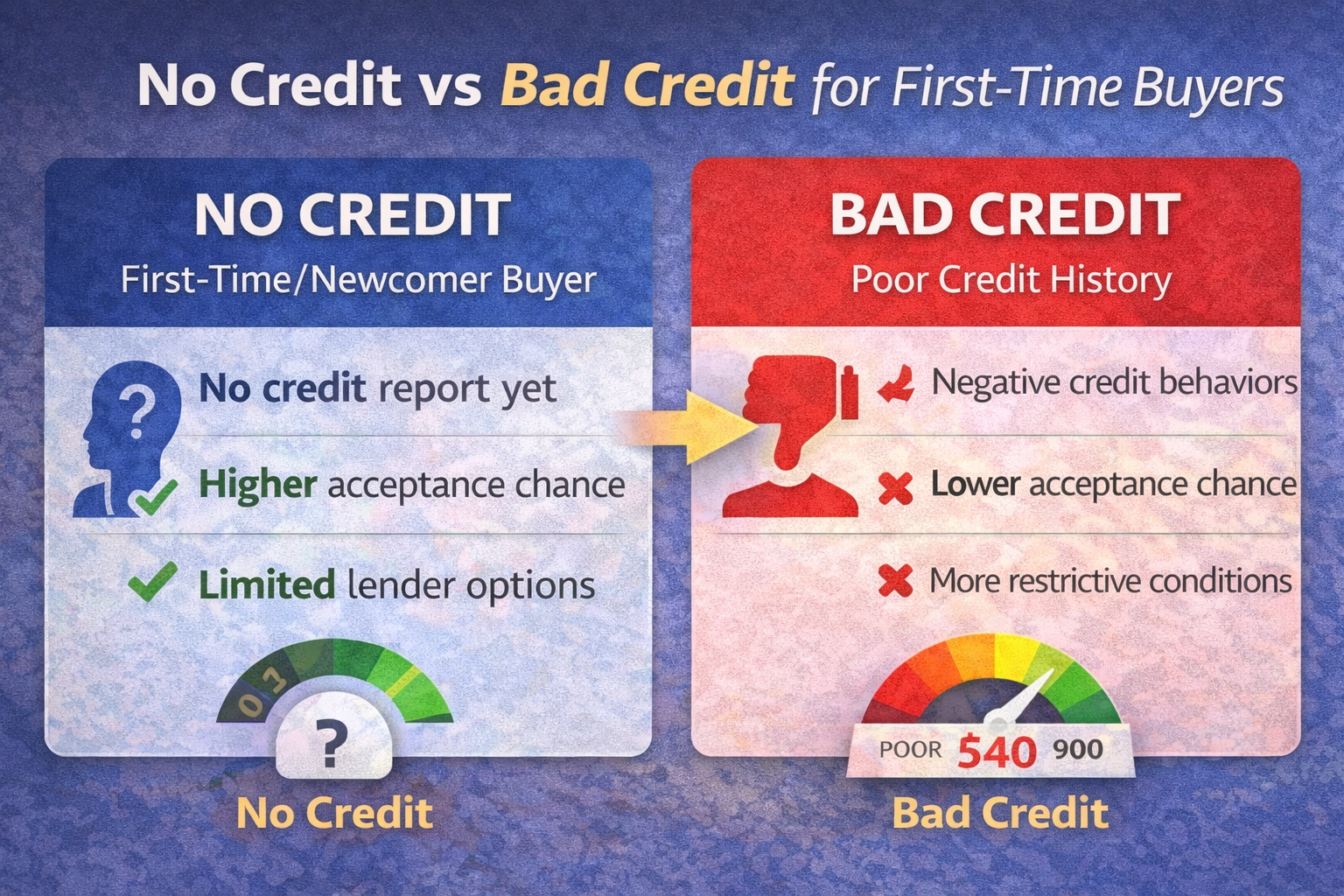

Can You Finance a Car With Bad Credit?

Yes, in some cases you can finance a car with bad credit.

A weak credit score can make the process harder, but it does not always end your options. Some buyers are approved even after past financial problems, especially when the rest of the application shows stability and the vehicle choice is realistic.

What usually changes when your credit is weaker

When a lender sees a weaker credit profile, they may still consider the file, but the structure of the financing often changes.

Common differences can include:

- higher interest rates

- fewer lender options

- closer review of income and debt

- requests for more supporting documents

- stronger importance placed on down payment

- tighter limits on vehicle choice or loan amount

That is why bad credit financing should not be judged only by whether approval is possible. The more important question is whether the final terms are realistic and manageable for your budget.

Situations where approval may still be possible

Approval may still be possible when the buyer has:

- stable full-time or consistent ongoing income

- enough income to support the proposed payment

- manageable existing debt

- a reasonable vehicle target

- a down payment

- signs of recent financial recovery or improved payment behaviour

In some cases, a co-signer may also help strengthen the file, though that should be approached carefully.

Why realistic budgeting matters even more with bad credit

When credit is weak, every part of the decision becomes more sensitive.

A higher rate can raise the monthly payment and the total loan cost. Insurance, maintenance, and repair costs may also add pressure after the loan begins. Before agreeing to a structure, it can help to test different payment scenarios with the finance calculator.

That is why buyers with bad credit should be especially careful not to focus only on getting approved. The better goal is to find a vehicle and payment structure that supports stable transportation without creating ongoing financial strain.

Bad credit does not mean you should rush into the first offer

Buyers with poor credit sometimes feel pressure to accept any approval they can get. Even if your options are narrower, it still helps to understand:

- the interest rate being offered

- the loan term length

- the estimated monthly payment

- the total amount to be repaid over time

- whether the vehicle itself is a sensible fit for your needs and budget

A calmer way to think about bad credit car financing

If your credit is weak, the most useful mindset is not embarrassment or panic. It is preparation.

Bad credit may limit flexibility, but it does not automatically remove all paths forward. What matters most is whether the financing fits your real situation in a sustainable way.

How Your Credit Score Can Affect Your Interest Rate and Monthly Payment

A credit score does not just affect whether you get approved. It can also affect how expensive the financing becomes.

That is an important difference. Many buyers focus on the yes-or-no part of the decision, but the real cost of the loan often matters just as much. A buyer with stronger credit may qualify for a more competitive rate, while a buyer with weaker credit may face a higher borrowing cost on the same vehicle.

Why the rate matters as much as approval

Interest rate affects both your monthly payment and the total amount you repay over time.

That means two buyers can finance vehicles at a similar price point and still end up paying noticeably different amounts. One may carry a payment that fits more comfortably into the budget. The other may be approved, but on terms that create more pressure month after month.

This is why approval by itself is not enough. A financing offer should also be reasonable.

How a higher rate changes the total cost

Even a modest increase in rate can raise the total cost of borrowing, especially over a longer loan term.

| Loan Example | Lower-Rate Scenario | Higher-Rate Scenario | What Changes |

|---|---|---|---|

| $10,000 used-car loan | Lower monthly payment | Higher monthly payment | More strain on monthly budget |

| $10,000 used-car loan | Less total interest paid | More total interest paid | Higher overall cost of the same vehicle |

| Same vehicle, same price | More room for insurance and maintenance | Less room for other ownership costs | Tighter long-term budget |

The main point is simple: a higher rate can make the same vehicle much less affordable over time.

Why monthly payment should not be the only focus

Monthly payment matters, but it does not tell the full story.

A loan can sometimes be stretched over a longer term to make the payment look easier. That can help in some cases, but it may also mean paying more interest overall. Buyers should try to understand both the payment and the total repayment, not just the number due each month.

A lower monthly payment is not always a better deal if the loan becomes more expensive in the long run.

What buyers should look at before saying yes

Before agreeing to a financing offer, it helps to review:

- the interest rate

- the monthly payment

- the loan term length

- the estimated total repayment

- whether the payment still leaves room for insurance, fuel, and maintenance

This is especially important for used-car buyers, because the vehicle may still need upkeep after the purchase. A loan should fit the full ownership budget, not just the financing approval.

What If You Have No Credit or Very Little Credit History?

Not every financing challenge comes from bad credit. Some buyers have no credit history at all, or only a very limited one.

That is an important difference. Bad credit usually means there is negative history on file. No credit or thin credit usually means the lender has less information to work with.

No credit is different from bad credit

A buyer with no credit history is not always seen the same way as a buyer with past missed payments or collections.

The challenge is not necessarily that the file looks negative. The challenge is that the lender may not have enough borrowing history to measure risk with much confidence.

That can still make approval harder, but it is a different kind of problem.

How first-time buyers may still improve their chances

Buyers with little or no credit history may still strengthen their application by focusing on the parts they can control.

That can include:

- stable income

- consistent employment

- a realistic vehicle choice

- a down payment

- manageable existing expenses

- a co-signer in some situations

A modest vehicle and a payment that clearly fits the budget may be easier for a lender to support than a more ambitious loan request.

A note for newcomers to Canada

Newcomers often face this issue because Canadian lenders may place more weight on local credit history.

That does not mean financing is impossible. It means the file may need stronger support from income, job stability, down payment, or a smaller loan amount.

For many buyers in this situation, the most helpful mindset is patience and preparation. Building Canadian credit takes time, but it can improve financing options later.

How to Improve Your Chances Before Applying for Car Financing

If you are thinking about financing a car, a little preparation can make a meaningful difference.

This does not mean you need a perfect score before you apply. It means you should strengthen the parts of your file that lenders are likely to notice. In many cases, small improvements in timing, budgeting, and documentation can make the application look more stable.

Check your credit before you shop

It helps to know where you stand before you start looking at vehicles.

Reviewing your credit can help you spot errors, understand your score range, and avoid surprises during the financing process. It can also help you set more realistic expectations about the kind of payment and loan structure you should target.

Pay down revolving balances if possible

High credit-card balances can put pressure on your file, even if your score looks acceptable at first glance.

If you can reduce revolving balances before applying, it may help show that your credit use is more manageable. Even a modest improvement can strengthen the overall picture.

Avoid taking on new debt right before applying

New debt can make your application look heavier and may reduce the room you have for another monthly payment.

If possible, avoid opening new credit accounts or making major financed purchases right before applying for a car loan.

Save a down payment

A down payment can help in more than one way. It can reduce the amount borrowed, lower the monthly payment, and make the file easier for a lender to support.

For some buyers, especially those with fair, weak, or limited credit, this can be one of the most useful steps.

Choose a realistic vehicle and payment range

One of the smartest things you can do before applying is to match your vehicle search to your actual budget. If you are close to taking the next step, you can also review the finance application page in advance.

A more modest vehicle that fits your income comfortably may create a much stronger financing file than a more expensive vehicle that leaves little room in the budget.

Gather your documents in advance

Having your documents ready can make the process smoother and show that you are prepared.

Common items may include:

- driver’s licence

- proof of income

- employment details

- proof of address

- banking information if required

- down payment proof if relevant

Preparation does not guarantee approval, but it can improve how clearly and confidently your application comes together.

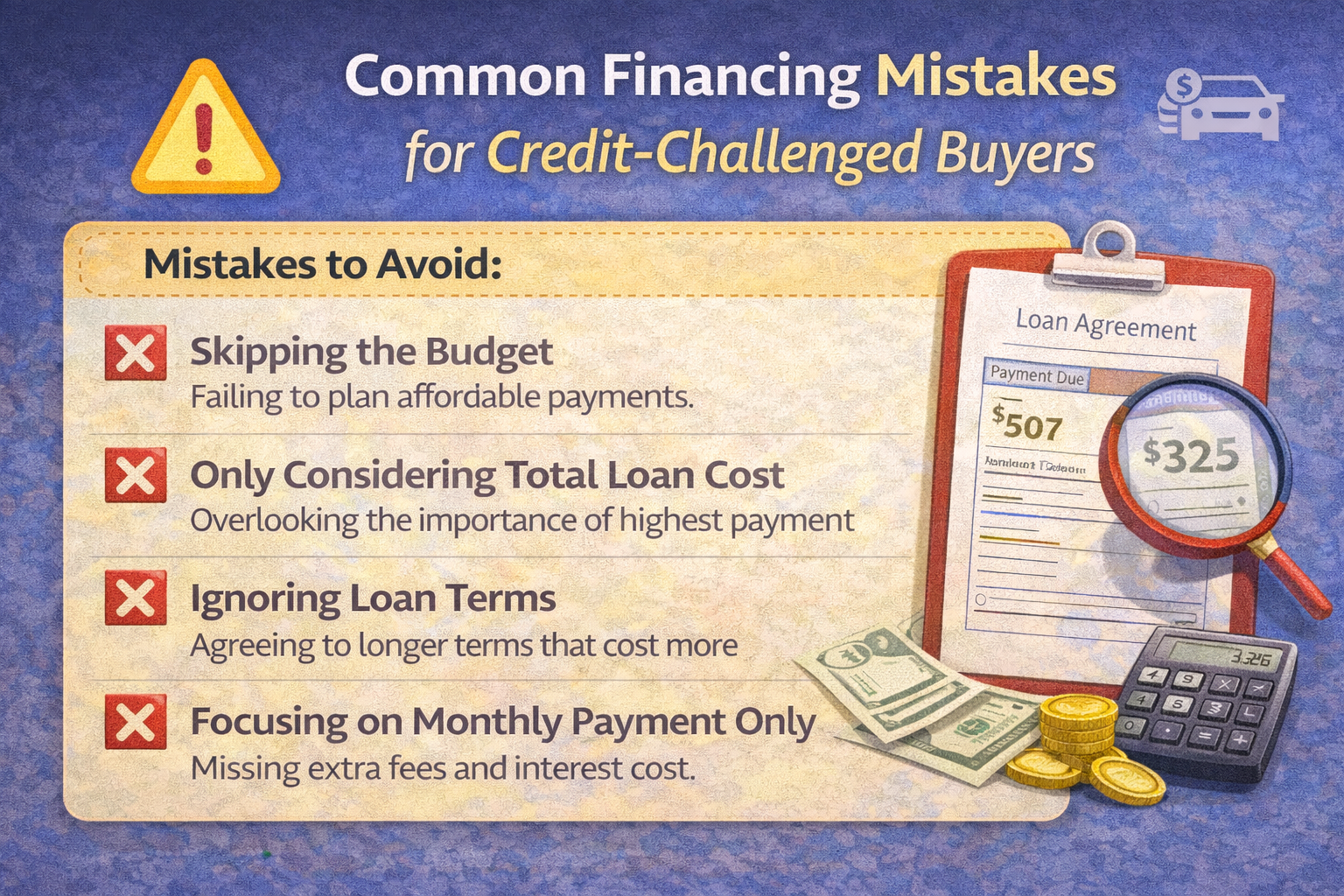

Mistakes to Avoid When Financing a Car With Fair or Poor Credit

When buyers feel pressure around approval, it becomes easier to make rushed decisions.

That is why this part matters. A financing application is not just about getting a yes. It is also about avoiding choices that create more financial stress later.

Focusing only on the monthly payment

Monthly payment matters, but it should not be the only number you look at.

A lower payment can sometimes come from stretching the loan over a longer term, which may increase the total amount repaid. It helps to look at the full cost, not just the monthly figure.

Ignoring the total cost of the loan

Two financing offers can feel similar at first, but become very different once you look at the total repayment.

A higher rate or longer term can make the same vehicle cost much more over time.

Applying everywhere at once

Multiple applications in a short period can make the process more confusing and may not help your position.

It is better to approach financing in a more organized way, with a realistic budget and a clear understanding of what you are trying to achieve.

Choosing too much car for your budget

A vehicle may be technically financeable without being financially comfortable.

Insurance, fuel, maintenance, and repair risk still matter after the loan begins. A more modest vehicle is often the safer long-term choice when credit is already under pressure.

Skipping questions about the terms

Before agreeing to financing, buyers should understand:

- the interest rate

- the monthly payment

- the loan term

- the total amount to be repaid

- whether the payment still fits the rest of the budget

A calm review of the terms can prevent expensive misunderstandings later.

How to Know Whether You Are Ready to Finance a Car

Not every buyer who can apply is truly ready to finance a vehicle.

That is not meant to be discouraging. It is simply a reminder that approval and readiness are not always the same thing. A financing decision makes more sense when the payment fits your life, not just the lender’s minimum requirements.

Signs you may be in a solid position

You may be in a healthier position to finance a car if you have:

- stable income

- manageable existing debt

- a realistic idea of your monthly budget

- enough room for insurance, fuel, and maintenance

- a practical vehicle target

- some savings or a down payment

These signs do not guarantee approval, but they usually mean the financing decision is being made from a more stable starting point.

Signs you may want to prepare first

In some situations, it may make more sense to pause and strengthen your position before taking on a loan.

That may be the case if you have:

- unstable income

- very high credit-card balances

- little room left after monthly bills

- no emergency cushion at all

- no clear idea of your total ownership costs

- a vehicle target that is beyond what your budget comfortably supports

Waiting is not always the right move, but it can be the smarter move when the budget is already under strain.

Why readiness matters more than urgency

Many buyers feel pressure to solve transportation needs quickly, and sometimes that pressure is real. Even so, it helps to step back and ask whether the financing choice is sustainable.

A vehicle should support your daily life, not make your finances harder to manage. That is why readiness matters. A more careful decision today can prevent ongoing stress later.

Financing a Used Car vs Financing a New Car: Does Credit Work Differently?

Your credit score matters in both cases, but the financing conversation is not always exactly the same.

The main difference is that with used cars, lenders may pay closer attention to the vehicle itself. Age, mileage, condition, and overall loan structure can matter more because the vehicle is an older asset with a different risk profile from a new car.

The score still matters in both cases

Whether you are financing a new or used vehicle, lenders still look at your credit profile, income, debt, and overall ability to repay.

A stronger score can still improve approval strength and rate options in either case. A weaker score can still lead to more caution, higher rates, or tighter conditions.

Why the vehicle may matter more with used cars

With a used vehicle, the lender is not only reviewing the borrower. They are also looking at a vehicle that may be older, have higher mileage, and carry different resale or long-term risk.

That can affect:

- which vehicles are easier to finance

- how much the lender is willing to finance

- how cautious the lender becomes about the loan structure

This is one reason used-car buyers should pay close attention to overall value, not just the sticker price.

Why used-car buyers should think in total-value terms

A used car can still be the smarter financial decision, especially when it offers a lower purchase price and avoids the steepest early depreciation.

But the right used car is not just one that gets approved. It should also make sense for your budget, expected ownership costs, and financing terms.

That is why used-car financing works best when the buyer looks at the full picture: credit profile, monthly payment, insurance, maintenance, and the condition of the vehicle itself.

Take the Next Step With Confidence

Once you have a clearer idea of what to look for, the next step is to turn that research into action.

You can

- Browse our current used car inventory,

- Explore financing options,

- Contact our team with questions,

- Or book an appointment or test drive.

Whether you are still comparing options or feel ready to move forward, taking the next step with a clear process can help you buy with more confidence and less guesswork.

FAQ

What is the minimum credit score to finance a car in Canada?

There is no single universal minimum credit score that applies to every lender. In many cases, buyers in the mid-600s and above are in a stronger position, but some financing may still be possible below that depending on income, debt, down payment, and the vehicle being financed.

Can I finance a car with a 600 credit score?

In some cases, yes. A 600 credit score may still be workable, especially if the rest of your application is stable. Income, job history, debt load, and vehicle choice can make a big difference.

Can I get a car loan with bad credit?

It may still be possible. A weaker credit profile can lead to higher rates and tighter conditions, but some buyers are still approved when the rest of the file is strong enough.

Does checking my credit score hurt it?

Checking your own credit is generally different from applying for new financing. Buyers should still review their situation carefully before applying, but it helps to understand where they stand before shopping.

Can a down payment help me get approved?

In some cases, yes. A down payment can reduce the amount being financed, lower lender risk, and improve the overall structure of the application.

Can I finance a used car with no credit history?

It may still be possible, but the lender may rely more heavily on income, job stability, down payment, or a co-signer. No credit is different from bad credit, but it can still make approval more cautious.

What else do lenders check besides credit score?

They may also look at income, employment stability, current debt, down payment, vehicle type, and past financial issues shown on the credit report.

Is it better to improve my score before applying?

In some situations, yes. Even modest improvements in credit use, debt levels, or down payment can strengthen the application. The right timing depends on how urgent the purchase is and how much your file could realistically improve.

Final Thoughts: Focus on Approval Strength, Not Just the Number

If you are asking what credit score do you need to finance a car, the most useful answer is that there is no one magic number.

A stronger credit score usually puts you in a better position, but it is not the only thing that matters. Lenders also look at income, job stability, debt pressure, down payment, and the vehicle itself. That is why some buyers with fair or weak credit still have options, while some buyers with better scores still need to be careful about what they take on.

The smarter goal is not just to get approved. It is to finance a vehicle on terms that fit your real budget and support reliable transportation without adding unnecessary strain.

If you are planning to move forward, the best next step is to review your credit, your budget, and your documents before you apply. You can start by exploring the finance application, comparing options in the inventory, or using the contact page if you want to ask questions before moving ahead.